Audit of the Implementation of Jordan’s Principle

Prepared by: Audit and Assurance Services Branch

October 2019

PDF Version (614 Kb, 41 Pages)

Table of contents

Acronyms

| ADM |

Assistant Deputy Minister |

|---|---|

| CA |

Contribution Agreement |

| CFRDO |

Chief Finances, Results and Delivery Officer |

| CFSR |

Child and Family Services Reform |

| CHRT |

Canadian Human Rights Tribunal |

| COI |

Conflict of interest |

| ESDPP |

Education and Social Development Programs and Partnerships |

| FAA |

Financial Administration Act |

| FNIHB |

First Nations and Inuit Health Branch |

| FTE |

Full Time Equivalent |

| INAC |

Indigenous and Northern Affairs Canada |

| ISC |

Indigenous Services Canada |

| MCF |

Management Control Framework |

| RO |

Regional Operations |

| SAP |

System Application Products |

| SOP |

Standard Operating Procedures |

Executive Summary

Context

Jordan's Principle began in 2007 as a parliamentary response to the death of Jordan River Anderson. Jordan passed away before being released from the hospital due to jurisdictional disputes within and between the federal and provincial governments over who would pay the costs for his in-home care. The Principle is a legal requirement; it is not a policy or program. It is a child-first initiative that calls for services to be delivered to First Nations children in their home communities and for government of first contact to ensure First Nations children can have equitable access to publicly funded services.

In 2016, the Canadian Human Rights Tribunal (CHRT) determined that Canada's approach to services for First Nations children was still discriminatory because it resulted in service gaps, service delays and service denials to First Nations children when accessing the support and services needed to achieve a normative standard of care and substantive equality with non-First Nations children. Achieving substantive equality for First Nations children is more than just providing equal access to health, education, and social supports and services; it's about providing the services required to support equal outcomes. The Government of Canada was ordered to immediately implement the full meaning and scope of Jordan's Principle.

The total approved budget for Jordan's Principle was $679.9M from 2016-2017 to 2018-2019. Budget 2019 proposed an investment of $1.2 billion in Jordan's Principle over the next three years to continue helping First Nations children obtain government products and services to address unmet needs. Approximately 90% of the Service Access Resolution Fund is being delivered through Contribution Agreements (CAs).

Why this is important

The implementation of Jordan's Principle is essential to ensuring that the Government of Canada meets the educational, social and health needs of First Nations children. The services and products provided by Jordan's Principle offers First Nations children the opportunity to achieve similar health, education, and social outcomes as other Canadian children.

Audit Objective and Scope

The Audit of the Implementation of Jordan's Principle used a two-phase approach. The two phases of the audit had different but complementary objectives and scopes, which were aimed at first assessing the initial risk related to the implementation of the Principle and then assessing the sustainability of the Principle by looking at key short-term and long-term practices needed to effectively implement the Principle. The following table outlines the objective and scope of each phase.

| Objective | Scope |

|---|---|

Provide a high level assessment of how the Department is managing the risks associated with the initial stages of the implementation of Jordan's Principle under the very tight timelines required by the CHRT. |

Activities related to implementation of Jordan's Principle within First Nations and Inuit Health Branch (FNIHB) and FNIHB -Regional Operations (RO) with a focus on FNIHB 's process for Jordan's Principle requests and basic financial processes, and on Jordan's Principle key short-term and long-term practices. |

| Objective | Scope |

|---|---|

Provide assurance that the Department has the key short-term and long-term practices needed for the implementation of Jordan's Principle and to fund government services, supports and products for First Nations children. |

Activities related to the Jordan's Principle implementation within multiple sectors; FNIHB , FNIHB -RO, Education and Social Development Programs and Partnerships (ESDPP), RO, Child and Family Services Reform (CFSR) and Chief key short-term and long-term practices. This audit phase did not consider areas of the Principle that are currently being developed and excluded the performance of the Department in meeting the timing requirements of the CHRT rulings. These elements may be considered in future audits. |

Statement of Conformance

The audit was conducted in conformance with the International Standards for the Professional Practice of Internal Auditing as supported by the results of the quality assurance and improvement program.

Conclusion

A unique challenge with Jordan's Principle has been the need to develop business processes while managing and delivering the Principle under tight deadlines and high pressure. Jordan's Principle is a unique initiative; therefore, a pre-existing model for its implementation is not available. In addition, a traditional period of design for the initiative is not available due to high demand and time constraints which resulted from implementation of the CHRT orders. Due to the changing landscape under which the Principle operates, the business processes and the definition and scope of what is required under Jordan's Principle have been continuously adapted to the CHRT orders.

In phase 1, the audit found that the Department has positioned itself to fully manage some of its risks related to the availability of information, communications with First Nations as well as financial practices including delegation of authority, Financial Administration Act (FAA) Section 34 and 33, and quality assurance reviews for payments. The employees and the follow-up they perform have helped the Department partially mitigate some of its information and knowledge risks.

In phase 2, the audit found that the Department had positioned itself to partially mitigate some of its risks related to the coordination and collaboration between all sectors involved in Jordan's Principle, identifying opportunities to address commonly occurring needs of First Nations children, ensuring that employees are equipped to respond to the variation and volume of Jordan's Principle requests, real and perceived conflicts of interest and building awareness of the importance of Jordan's Principle to all Canadians. The Department has not fully implemented the mitigation measures that they identified to oversee the monitoring and reporting requirements in the contribution agreements.

The audit team identified recommendations to address the remaining risks to the Department.

Recommendations

- Going forward, the Senior Assistant Deputy Minister (ADM) of FNIHB should ensure that information stored in multiple locations is consolidated into the request file. This will allow information to be found more easily in the future.

- While there is a strong sense of urgency to make a decision within the timelines mandated by the CHRT, the timelines stop once the decision is communicated. The Senior ADM of FNIHB should ensure that a post-decision review of file completeness is performed to ensure that information required by management in the Standard Operating Procedures is present and accessible for future reference.

- The Senior ADM of FNIHB , with support from the CFRDO, should implement a monitoring process to ensure that FAA Section 32 commitments are being input into System Application Products after the decision has been communicated and that unused funds are released after final payment. The results of the monitoring should be addressed through corrective action as required.

- The Senior ADM of FNIHB in consultation with ESDPP, CFRDO, CFSR and RO should formally define and communicate roles, responsibilities and accountabilities for all sectors involved to ensure efficient coordination of their approach to implementing Jordan's Principle.

- The Senior ADM of FNIHB should leverage data trends to proactively identify alternative ways to provide commonly requested products and services through existing or new programs.

- The Senior ADM of FNIHB should adopt a risk-based approach to the oversight of reporting and monitoring the external use of funds through Jordan's Principle.

- The Senior ADM of FNIHB , in consultation with all involved sectors, should provide additional assistance to employees to better equip them to respond to the increase in volume and variation in Jordan's Principle requests by finalizing and implementing the Wellness Plan and by providing global feedback and lessons learned throughout the adjudication process.

- The Senior ADM of FNIHB should formalize the existing internal conflict of interest practices specific to Jordan's Principle's operational context.

- The Senior ADM of FNIHB , in consultation with Communications, should work towards developing and implementing a communication strategy to directly target the wider population to build awareness of the importance of Jordan's Principle.

Management Response

Management is in agreement with the findings, has accepted the recommendations included in the report, and has developed a management action plan to address them. The management action plan has been integrated into this report.1. Background

The Audit of the Implementation of Jordan's Principle was approved in the Crown-Indigenous Relations and Northern Affairs Canada and Indigenous Services Canada (ISC) 2018-19 to 2019-20 Risk-Based Audit Plan on August 21, 2018. Internal Audit began the Audit of the Implementation of Jordan's Principle with a two phased approach. Phase 1 started in November 2018 while phase 2 started in February 2019.

The audit key results and recommendations for each of the audit phase will be presented in this report under two separate sections.

2. Context

Jordan's Principle began in 2007 as a parliamentary response to the death of Jordan River Anderson. Jordan passed away before being released from the hospital due to jurisdictional disputes within and between the federal and provincial governments over who would pay the costs for in-home care. The Principle is a legal requirement; it is not a policy or program. It is a child-first initiative that calls for services to be delivered to First Nations children in their home communities and for government of first contact to ensure First Nations children can have equitable access to publicly funded services.

In 2016, the Canadian Human Rights Tribunal (CHRT) determined that Canada's approach to services for First Nations children was discriminatory because it resulted in service gaps, service delays and service denials to First Nations children when accessing the support and services needed to achieve a normative standard of care and substantive equality with non-First Nations children. Achieving substantive equality for First Nations children is more than just providing equal access to health, education, and social supports and services; it's about providing the services required to support equitable outcomes. The Government of Canada was ordered to immediately implement the full meaning and scope of Jordan's Principle.

On July 5, 2016, the Government of Canada announced an initial three year investment of $382.5 million ($88.8M in 2016-2017, $138.0M in 2017-2018, and $155.7M in 2018-2019) to immediately address health, social and education services, supports and products through Jordan's Principle. Due to increased demand for services through Jordan's Principle, an additional $297.4M in off-cycle funding was approved in 2018-2019 to address the pressures, bringing the total approved budget for Jordan's Principle to $679.9M over three years. Budget 2019 proposed an investment of $1.2 billion in Jordan's Principle over the next three years to continue helping First Nations children obtain government products and services to address unmet needs. Approximately 90% of the Service Access Resolution Fund is being delivered through Contribution Agreements (CAs).

2.1 Key Orders and Requirement

Jordan's Principle is a legal requirement resulting from the 2016 CHRT decision. Since the initial CHRT decision, several subsequent CHRT orders regarding how Jordan's Principle should be defined and implemented were issued. In its May 26, 2017 ruling (amended November 2017), the CHRT provided additional clarity vis-à-vis Jordan's Principle. It outlined that Jordan's Principle:

- Applies to all First Nations children, no matter where they live;

- Ensures there are no gaps in publicly funded services for First Nations children;

- Does not require the presence of a jurisdictional dispute to be applied; and,

- Requires that Canada consider funding services and supports not available to other children if those services/supports would enable substantive equality, be culturally appropriate and/or in the best interest of the child.

In February 2019, the CHRT issued an interim relief order for Jordan's Principle stating that in urgent and/or life-threatening situations, non-status First Nations children who live off-reserve (but are recognized by their First Nation) will be covered based on the child's best interests. This interim relief order will be in effect until the issues regarding the definition of a First Nations child and the impact of status on eligibility are adjudicated at a full hearing. Canada has asked the Panel to dismiss the motion and the Interim Order. Canada is still waiting for the results from these hearings.

The CHRT mandated specific timeframes for the Department to address Jordan's Principle requests. The timeframes begin once all the information required to make a decision has been received. The timeframes outlined in the CHRT orders are different based on the urgency of the request and if the request is for an individual or for a group. The timeframes are:

- 12 hours for urgent individual requests;

- 48 hours for non-urgent individual requests and urgent group requests;

- 7 calendar days for non-urgent group requests; and,

- Immediate referral to emergency authorities for cases where the denial or delay of a service could reasonably result in significant and/or irremediable harm to a child who is the subject of the request. This applies to individual and group service requests.

2.2 Jordan's Principle Implementation

Multiple sectors work together to deliver Jordan's Principle within ISC. They include First Nations and Inuit Health Branch (FNIHB), FNIHB -Regional Operations (RO), Education and Social Development Programs and Partnerships (ESDPP), RO, Child and Family Services (CFSR) and Chief Finances, Results and Delivery Officer (CFRDO).

Within the FNIHB regional offices and RO (British Columbia (BC) region), there are focal points that are responsible for receiving requests, reviewing the information, and making a decision within the mandated CHRT timelines. If the request cannot be approved or requires additional clinical consultation, the request must be escalated to FNIHB Headquarters where a decision will be made by the Assistant Deputy Minister (ADM) of FNIHB -RO.

As of April 1, 2019, the majority of the responsibility for adjudicating Jordan's Principle request was transferred to FNIHB regional offices.

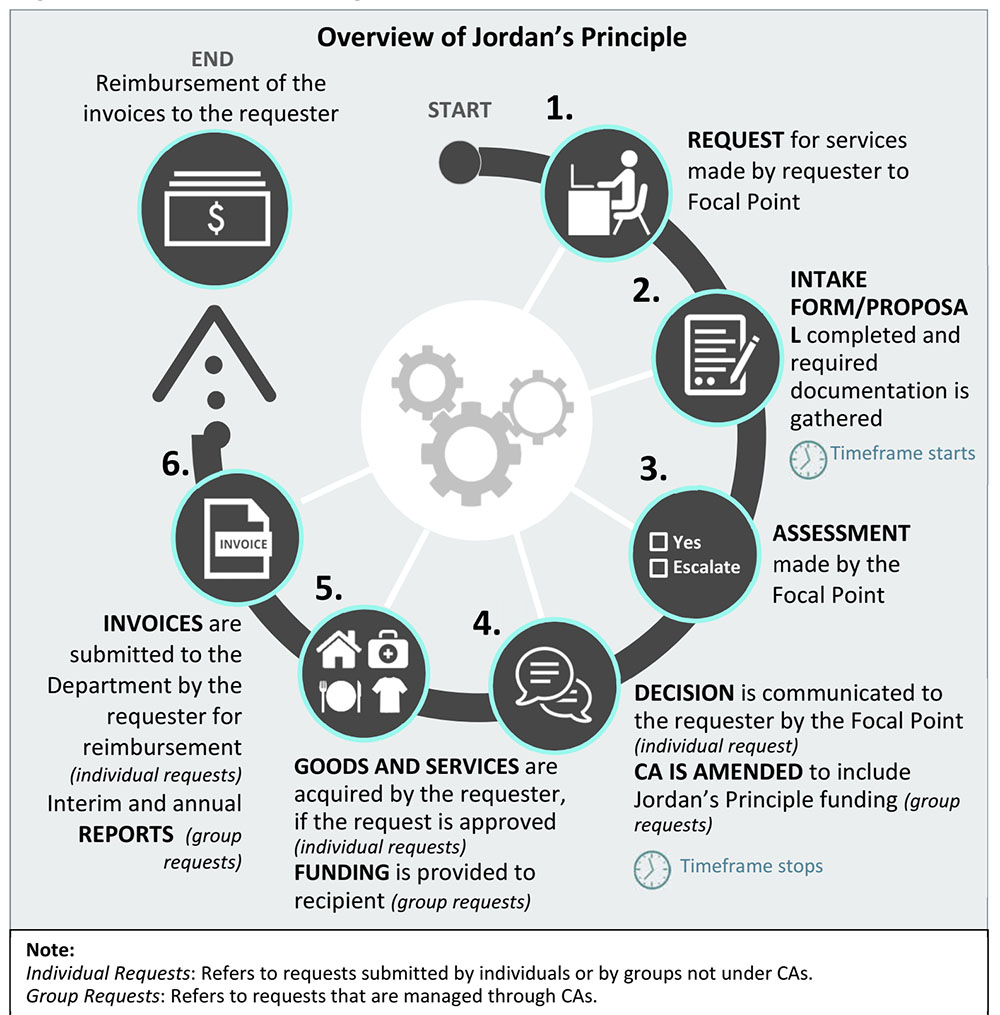

Figure 1 - Process for making a decision on product or service requests

Text alternative for Figure 1 - Process for making a decision on product or service requests

Figure 1 illustrates the adjudication process for making a decision on goods or services requests under Jordan’s Principle. The figure differentiates between individual and group requests. Individual requests are requests submitted by individuals or by groups not under CAs. Group Requests are requests that are managed through CAs. The adjudication process is divided in six steps. Step one is described as the request for services being made by the requester to the Focal Point. Step two is described as the intake form or proposal being and the documentation being gathered. Step three is described as the assessment made by the Focal Point. For individual requests, step four is described as the decision being communicated to the requester by the Focal Point. For group requests, step four is described as contribution agreement being amended to include Jordan’s Principle funding. For individual requests, step five is described as goods and services being acquired by the requester if the request is approved. For group requests, step five is described as funding being provided to the recipient. For individual requests, step six is described as invoices being submitted to the Department by the requester for reimbursement. For group requests, step six is the interim and annual reports. The adjudication process ends when the invoices are reimbursed to the requester.

2.3 Tools in Place for Jordan's Principle

The Jordan's Principle Division of FNIHB has developed Standard Operating Procedures (SOP) which are contained in an evergreen document that summarizes the steps to process requests for products and services for eligible First Nations children. The SOP has also evolved to reflect the current business practices required by the changing operational context.

A Management Control Framework (MCF) for Jordan's Principle is near completion, with action plans that evolve to align with the ongoing changes to the set of priorities and CHRT orders. The MCF will help to achieve the Principle's strategic, operational, reporting, and financial objectives. The MCF action plan focuses on key areas such as:

- Governance;

- Metrics and Expected Results;

- Data Collection and Monitoring;

- People Management; and,

- Operational and Financial Control Processes.

Furthermore, Synergy in Action, the business intelligence group within FNIHB , has been mandated to modernize the processes and systems used in the delivery of Jordan's Principle. As of June 2019, the mapping of Jordan's Principle decision-making process for every region, in addition to Headquarters, has been completed. This was part of a table top exercise in order to present and validate future proposed processes and systems basic capabilities.

3. Phase 1

3.1 Objective and Scope

Audit Objective

The objective of the first phase of this audit was to provide a high-level assessment of how the Department is managing the risks associated with the initial information gathering, decision-making, and financial management stages of Jordan's Principle. The audit focused on how the Department is managing its risks as it implements Jordan's Principle under the very tight timelines required by the CHRT.

Audit Scope

The scope of phase 1 focused on the work of FNIHB and CFRDO from the receipt of a request (CAs individual and group) to the decision-making and communication processes. It also looked at basic financial processes such as the initial commitment of funds to the processing of the payments.

This phase of the audit covered the activities related to the Jordan's Principle implementation within FNIHB and FNIHB -Regions (Headquarters and in the Department's regional offices).

3.2 Audit Approach and Methodology

The audit team obtained and analyzed sufficient information and evidence to provide assurance in support of the audit conclusion. Additional information on the audit coverage is provided in the Appendix A: Audit Criteria.

The audit methodology included:

- Review of documentation related to the management of Jordan's Principle;

- Interviews with key employees in Headquarters and the Ontario, Northern and Manitoba regional offices ;

- Walkthroughs with key employees in Headquarters and the Ontario, Northern and Manitoba regional offices; and,

- Testing of a sample of Jordan's Principle files in Headquarters and the Ontario, Northern and Manitoba regional offices.

A judgmental sample of 310 Jordan's Principle files was tested in phase 1. The sample included approved, denied, and escalated files for both individual and group requests. The sample covered the 2017-2018 and 2018-2019 fiscal years up to September 30, 2018. The purpose of the file testing was to generate illustrative and practical evidence of the types of issues/challenges encountered in delivering Jordan's Principle within the regions.

4. Phase 1 - Key Results and Recommendations

4.1 Information Available for Future Reference

To respect the timelines mandated by the CHRT, the Principle has been managed and delivered at the same time as the appropriate business processes were being developed. To put the needs of First Nations children first, the early business processes focussed primarily on decision-making and less on the administrative aspects of the Principle.

As the delivery of the Principle matured, management developed the SOP. Requests under Jordan's Principle are to include sufficient information for the regional Focal Points to consider a request as complete and to make a decision.

The request file should include details of the individuals involved, the products or services requested, complete costing information and the reason for the request. Additional information may include letters of support from professionals, a professional assessment or diagnosis, and details on the child's eligibility for product and services under Jordan's Principle.

Risk

As of January 2019, ISC made decisions on over 209,000 approved requests (individuals and groups). There may be a future need to refer back to the request files to understand the nature of the requests that were made and how those requests were supported. There is a risk that insufficient information about the requests has been documented in the files for future reference by the Department.

Required information to Assess a Request

When the Department receives a request under Jordan's Principle, basic information about the request is provided. Individual requests require information on the identity of the child, date of birth, status information. It also requires information about the request such as the rationale, the support from a professional (e.g. assessment or diagnosis), as well as the cost and frequency of the support or service. If the focal point determines that there is not enough information provided, a follow-up is performed. Group requests require similar information but with less specific information about the children.

Findings

Group requests administered under Contribution Agreements (CA)

For the group requests that are governed by a new or a pre-existing CA, the level of information in the file met the requirements of management's SOP. The requests were supported by proposals that provided details on the specific activities, including the number of children to be helped, reason for requesting Jordan's Principle funding and proposed outcomes.

Individual and group requests

For half the individual requests in the sample as well as group requests that did not require a CA, the information in the file did not meet the full requirements identified in management's SOP. The intake forms were not consistently completed and supporting documentation was not always on file. Types of missing information included the information needed to identify the products or services requested and the reason the request was made. Specific examples of missing information included:

- An explanation of how orthodontic treatment was meeting the comparable provincial or territorial or Non-insured health benefits standards for dental care;

- The rationale behind the request for services in a residential treatment centre; and,

- Why a vehicle "conversion kit" was required to make the vehicle wheelchair accessible.

How the Risks are Being Managed

Employees

Some of the employees that are responding to Jordan's Principle requests have a significant amount of corporate knowledge related to the Principle's history as well as the request files. The risk of not finding the required information in the file is partially offset by employees who are familiar with the files. For example, during the field work portion of this audit, the team requested information related to a specific request identified only by its reference number. The employee in the next cubicle overheard the request and jumped in to provide the name of the person who had made the request and an impromptu history of previous requests and the nature of the current request. The commitment and dedication of the employees involved in Jordan's Principle should be recognized as a key asset in managing departmental risk. However, over-reliance on this type of ‘corporate memory' carries longer term risks when there are inevitable changes in personnel over time.

A generic email box is uses to receive information from requestors who are submitting requests, providing additional information or responding to correspondence. The emails in the generic mailbox are identified with the associated request number assigned by the Department. The risk of not finding information in the request file is partially mitigated by the emails that are stored in the generic mailbox. These emails contain some of the additional information that is missing from the request file.

These emails were sometimes saved in the request file which is a good practice. When the email files could be opened, the additional information that they contained often addressed the gaps in the request files. However, several instances of the saved email files being corrupted were observed. Not only was the additional information lost, the corrupted files created an erroneous impression that the information in the file was fairly complete.

Recommendations

1. Going forward, the Senior ADM of FNIHB should ensure that information stored in multiple locations is consolidated into the request file. This will allow information to be found more easily in the future.

2. While there is a strong sense of urgency to make a decision within the timelines mandated by the CHRT, the timelines stop once the decision is communicated. The Senior ADM of FNIHB should ensure that a post-decision review of file completeness is performed to ensure that information required by management in the Standard Operating Procedures is present and accessible for future reference.

4.2 Defending Decision Made

External parties that are not familiar with Jordan's Principle might find it difficult to understand the exact nature of the services and support provided to First Nations children. Management's SOP requires that the decision made for the request and the rationale to support that decision are included in the file.

Risk

Jordan's Principle operates under significant external scrutiny including from the CHRT. It is expected that the level of public interest will increase as Jordan's Principle becomes more widely known. The Department may be required to defend or explain decisions that it has made with respect to requests. There is a risk that the documentation around the decision-making process is not sufficient to explain the decisions made.

Findings

Management's SOP provides the criteria for regional employees to evaluate and approve a request or to escalate it to Headquarters when recommended for denial or for consideration and decision. Headquarters makes the determination and it is forwarded to the ADM for review. The evaluation considers whether the request should be provided to ensure:

- Substantive equality in the provision of products and/or services to the child;

- The cultural appropriateness of products and/or services; and,

- The best interests of the child are safeguarded.

Overall, the sampled files did not include documentation to support the approval or denial. The rationale for the decision, the evaluation of the services requested and the analysis of the cost related to that service were not available in the file.

For example:

- A request was made for a behavioral therapist and a behavioral consultation. The amount approved was less than the amount requested. There was no analysis in the file to explain why the request was not fully funded.

- A group request was made for several different types of healthcare workers. The amount required for salaries was provided as a lump sum. There was no breakdown of costs in the file to support any analysis.

How the Risks are Being Managed

The risk of not being able to explain decisions made under Jordan’s Principle is partially mitigated by regional employees who use their judgement in their decision-making. These employees are experienced with Jordan’s Principle and are familiar with many known service gaps for First Nations children (e.g. psychological assessments, child and youth mental health counselling and psychotherapy as well as speech and language therapy).

Recommendation

See recommendation 2. The post-decision review of file completeness will also confirm that the rationale, evaluation, and analysis required by management's Standard Operating Procedures are present in the file. This will support the Department in explaining decisions it has made for Jordan's Principle.

4.3 Timely Communication with First Nations

There is a strong sense of urgency in the Department to ensure that requests are processed and decisions are made within the mandated timelines. Despite the urgency, service delivery to First Nations is a key element of ISC's mandate that needs to remain a priority.

Risk

There is a need to respect the mandated timelines for Jordan's Principle. There may be a risk that decisions are not being communicated in a timely manner to requestors or that the terms of the decisions are not communicated consistently.Findings

Management's SOP requires that all decisions be provided immediately to the requester whether it is for an approved or denied product or service request.

Overall, for the sampled files, the decision made for the request was communicated in a timely manner. The decision was always shared using emails which were often followed up by a formal letter. When both emails and a formal letter were used, the conditions set out for the approved requests were consistent between the two (CAs no inconsistencies were found).

4.4 Financial Practices

Jordan's Principle funding is to be managed and delivered consistently with the Financial Administrative Act (FAA) and the Treasury Board Policy on Financial Management which provides key responsibilities for Deputy Ministers, Chief Financial Officers, and Senior Departmental Managers to ensure that decisions are made by employees with proper delegated authority.

Financial Delegation

Financial authority is established by the financial delegation of authority instrument. Any decision to approve requests for funding, reimbursement of invoices, or flow funds under CAs requires the appropriate level of authority.

Risks

The speed required to approve requests within the mandated timelines increases the risk that the approver may not have a sufficient level of financial authority.

Findings

Overall, for the sampled files, financial decisions were made by employees with appropriate delegated financial authority. Despite the turnover in management positions within the regions, the individual approving the request had the appropriate delegated financial authority. Moreover, individuals exercising FAA Section 34 and 33 approvals also had the appropriate delegated financial authority.

Financial Commitments and Payments

Funds commitment

FAA Section 32 provides the authority to commit funds against an appropriation before an expense is incurred. After the expense is incurred and the final payment is made, the unused commitment should be released so that it becomes available for other requests. Not only does it demonstrate the Department's fiscal responsibility but it also supports the monitoring required to track how much of the Department's funds are committed to be spent on Jordan's Principle.

Risk

The funding for Jordan's Principle is a significant portion of ISC's budget. Also, regions are noticing a higher demand for products and services requested under Jordan's Principle as First Nations become more aware of it. Given the current departmental funding pressures, there is a risk that management may be challenged to accurately determine funds committed under Jordan's Principle.Findings

Management's SOP states that the appropriate FAA Section 32 instrument must be signed as soon as a request is approved and that compliance to the Act applies as soon as the funding commitment is made.

For group requests that require a CA, the financial information is input into the Grants and Contributions Information Management System. The system feeds SAP, the Department's financial management system, and automatically updates the financial commitments.

For individual requests, a variety of processes were observed to commit funds. The Ontario Regional Office creates yearly bulk commitments for each type of service. In the Manitoba Regional Office and the Northern Regional Office, commitments are sometimes created just prior to payment of the invoice. Other times, commitments are recorded when confirmation of the vendor is received. Despite the different processes in place, financial commitments were not consistently made immediately after the request was approved.

Recommendation

3. The Senior ADM of FNIHB , with support from CFRDO, should implement a monitoring process to ensure that FAA Section 32 commitments are being input into SAP after the decision has been communicated and that unused funds are released after final payment. The results of the monitoring should be addressed through corrective action as required.

Payment claims

The challenges created when meeting the mandated timelines for decision-making can also create challenges in supporting the payment process.Risk

The volume of payments for Jordan's Principle is significant. There is a risk that a request for payment may not be fully supported by appropriate financial documentation.

Findings

The Department has developed and established a Jordan's Principle Financial Claims Process to expedite payments and ensure that financial controls are in accordance with the FAA. This claims process is mandatory and was communicated to the Accounting Hub where the release of payments is processed.

In 2018-2019, the Accounting Hub introduced a Quality Assurance Review process that is performed prior to releasing payments. As part of the Quality Assurance Review process, errors in the payment request are flagged and corrected. The Accounting Hub developed an "Issue Tracker" to provide feedback to Jordan's Principle on common issues. This Quality Assurance review process ensures that payments are appropriately supported and do not exceed the committed funds.

5. Phase 2

5.1 Objective and Scope

Audit Objective

The objective of phase 2 of the audit was to provide reasonable assurance that the Department has the key short-term and long-term practices needed for the implementation of Jordan's Principle and to fund publicly funded services, supports and products for First Nations children.

Audit Scope

The scope of phase 2 included an examination of Jordan's Principle's key short-term and long-term strategy, including how the Department is positioning the Principle to ensure the needs of First Nations children continue to be met with wide support for the Principle and by developing means to proactively address service gaps. The audit covered the activities related to the Jordan's Principle implementation within multiple sectors including FNIHB , FNIHB -RO, ESDPP, RO, CFSR and CFRDO.

This phase of the audit did not consider areas of the Principle that were currently being developed at the time of the audit such as the MCF action plan and the operational business management process review. The audit also excluded the performance of the Department in meeting the timing requirements of the CHRT rulings. This information is already monitored by the Department as well as external parties. These elements may be considered in future audits.

5.2 Audit Approach and Methodology

The audit team obtained and analyzed sufficient information and evidence to provide assurance in support of the audit conclusion. Additional information on the audit coverage is provided in the Appendix A: Audit Criteria.

The audit methodology included:

- Review of documentation related to the management of Jordan's Principle;

- Interviews with key employees working in sectors included in the scope of the audit in Headquarters and regional offices (CAs Ontario, Manitoba and Saskatchewan);

- Testing of a sample of Jordan's Principle request files managed under CAs (CAs Ontario, Manitoba and Saskatchewan).

In phase 2, a judgmental sample of 81 Jordan's Principle requests were tested to determine if reporting and monitoring was completed as defined by CAs requirements, how management is obtaining reports from recipients and how this information is being used for performance management, risk management and decision-making. The audit sample covered the 2017-2018 and 2018-2019 fiscal years and included approved request files managed under CAs.

6. Phase 2 - Key Results and Recommendations

6.1 Sustainability of Jordan's Principle

Coordination and Collaboration

In August 2017, there was a dissolution of Indigenous and Northern Affairs Canada (INAC) which resulted in the formation of two new Departments, Indigenous Services Canada and Crown-Indigenous Relations and Northern Affairs Canada. As part of the Government of Canada transformation, FNIHB was transferred from Health Canada to the new Department of ISC.

For the first two years of the implementation of Jordan's Principle, and prior to FNIHB 's move to ISC, each Department (CAs Health Canada and the former INAC) had dedicated teams sharing the responsibilities of administering and delivering Jordan's Principle. The adjudication of Jordan's Principle requests took place at the regional offices of both FNIHB and RO. FNIHB 's responsibilities focused on requests related to health, and RO Sector of the former INAC was responsible for requests related to the social and educational needs of First Nations children.

As of April 1, 2019, the majority of the responsibility for adjudicating Jordan's Principle requests was transferred to FNIHB regional offices. Due to the change in responsibility, FNIHB and RO have been working together to support the transfer of existing files and RO is referring new requests received pertaining to social and education programs to the FNIHB regional offices.

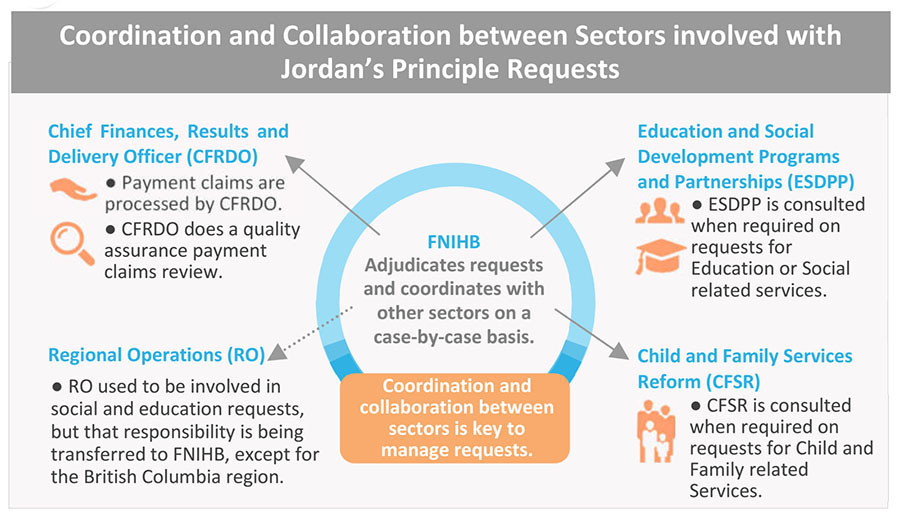

While FNIHB is taking the lead responsibility for adjudicating Jordan's Principle requests and ultimately will be accountable for decisions made on these requests, other sectors and/or programs (e.g. ESDPP, CFSR, RO, CFRDO) are involved in the delivery of Jordan's Principle. Figure 2 illustrates the sectors involved in delivering Jordan's Principle and their respective roles.

Figure 2: Coordination and Collaboration

Text alternative for Figure 2: Coordination and Collaboration

Figure 2 illustrates the coordination and collaboration between Sectors involved with Jordan’s Principle Requests which is key to manage requests. FNIHB is located in the center as this sector is taking the lead responsibility for adjudicating Jordan's Principle requests. They adjudicate requests and coordinate with other sectors on a case-by-case basis. Firstly, The Education and Social Development Programs and Partnerships (ESDPP) is consulted when required on requests for Education or Social related services. Secondly, the Child and Family Services Reform (CFSR) are consulted when required on requests for Child and Family related Services. Thirdly, Regional Operations (RO) used to be involved in social and education requests, but that responsibility is being transferred to FNIHB , except for the British Columbia region. Lastly, Chief Finances, Results and Delivery Officer (CFRDO) are responsible for processing payment claims and performing quality assurance payment claims review.

Risk

Given the number of sectors involved in Jordan's Principle and the prominent role of FNIHB , there is risk that the health perspective may take priority over social and educational perspectives in decision-making and in the strategic direction of the Principle.

Findings

The audit team was informed by regional employees that efforts are being made to support coordination and collaboration at the regional operational level between FNIHB , FNIHB -RO, RO, ESDPP, CFSR and CFRDO. FNIHB employees working on Jordan's Principle requests are reaching out to their colleagues in other relevant sectors to obtain advice on an ad-hoc basis to support service delivery. For example, FNIHB employees will reach out to verify with a program if funding is available under their authority to support a request. FNIHB 's Jordan's Principle employees indicated that they face certain challenges in receiving timely responses from other sectors when requesting information. This is driven by the fact that other sectors may not see the same timeframes outlined in the CHRT orders, as applicable to them for adjudicating Jordan's Principle requests, and moreover, other sectors may have their own workloads which may hinder their ability to provide a timely response.

The roles, responsibilities and accountabilities of all departmental sectors involved in supporting the delivery of Jordan's Principle have not been clearly defined, formalized and/or communicated in the formal documents supporting Jordan's Principle (CAs, MCF and SOP). The SOP for Jordan's Principle does not set clear expectations related to the roles, responsibilities, and authorities of the sectors involved. The MCF action plan includes an expectation that "roles, responsibilities and accountabilities of key players and organizations are appropriately aligned with one another and cover all key functions" but roles and responsibilities have not been defined. Defined roles and responsibilities reduce inefficiencies in resource utilization and overlaps and/or duplication of funding provided by existing ISC programs for the same services and/or products, which helps to ensure the sustainability of Jordan's Principle.

The Department has established several working groups and committees (e.g. Jordan's Principle Oversight Committee, MCF Advisory Committee, bi-weekly Focal Point meetings, etc.) that include representatives from various ISC sectors that support the governance and direction of Jordan's Principle. While several ISC sectors are invited to participate at these committees, participation is inconsistent.

Recommendation

4. The Senior ADM of FNIHB in consultation with ESDPP, CFRDO, CFSR and RO should formally define and communicate roles, responsibilities and accountabilities for all sectors involved to ensure efficient coordination of their approach to implementing Jordan's Principle.

Leveraging Data

During the first two years of implementation, Jordan's Principle focused on respecting timelines mandated by the CHRT and managing the significant increase in the volume of Jordan's Principle requests (refer to figure 3). As such, business processes that govern the implementation of Jordan's Principle were being developed while the Principle was being delivered under tight timelines. Fiscal year 2018-2019 was the first year where any significant data analysis and reporting took place for Jordan's Principle. The main purpose for the Department's data collection for Jordan's Principle was to report to Treasury Board and to show compliance with CHRT rulings.

Risk

There is a risk to the sustainability of Jordan's Principle funding as it is being used for products and services that are or should be covered under existing ISC programs, Provincial programs or other areas (CAs offsetting funding due to underfunding).

Findings

While there are data collection processes in place to support FNIHB regional offices in performing national reporting as it relates to Jordan's Principle, there is limited use of this information in planning and decision-making. FNIHB regional offices are collecting data in an Excel-based data tracker with a main focus on outputs as opposed to outcomes.

Currently, the Department funds a range programs and services for health, social and education to First Nations children under Jordan's Principle. The Department has acknowledged that the maturity level of data collection and analysis is not sufficient to quantify cross program impact, to reinvest available funds or to inform long-term policy and ISC program decisions. By using existing information and by conducting trend analysis, the Department could identify current gaps in available programs and services and, in turn, determine the sustainability of the departmental support to children. This analysis could also help other programs better understand the role and outcomes of Jordan's Principle.

Subsequent to the audit, Internal Audit noted that there have been recent and planned improvements at the FNIHB national level for data collection and analysis, such as:

- Building a Case Management System for Jordan's Principle nationally lead by the Department's in-house business intelligence unit; and,

- Jordan's Principle National team is updating its Annual Reporting template (called the Data Collection Instrument).

Recommendation

5. The Senior ADM of FNIHB should leverage data trends to proactively identify alternative ways to provide commonly requested products and services through existing or new programs.

Contribution Agreements

Requests under Jordan's Principle for products and services are made on behalf of individuals or groups of children. Group requests are considered most appropriate when the needs of children seeking services are more effectively met in the context of the collective needs of a defined group. For fiscal year 2018-2019, group requests comprised approximately 90% of the total Jordan's Principle expenditures on products and services.

Requests managed under CAs are not specific to Jordan's Principle. The CAs are developed for the recipient and include various programs and initiatives within ISC through which the recipient can get funding. As required under their CAs, recipients must periodically report on the actual number of children and the products and services received through their service delivery.

Furthermore, the Treasury Board Policy on Transfer Payments dictates that administrative requirements on recipients should be proportionate to the risk level. In particular, monitoring, reporting and auditing should reflect the level of risk, the value of funding in relation to administrative costs, and the risk profile of the recipient.

At a departmental level, the current SOP lay out the following expectations:

- Jordan's Principle has efficient and meaningful mechanisms to monitor its financial and operational performance at the regional and national levels; and,

- Mechanisms exist to follow up and confirm that products and services are delivered as intended, with the intended results.

Further to the SOP, the draft MCF has positioned monitoring as a key activity to facilitate course correction, continuous improvement and more fulsome external reporting.

Risk

The Department's approach to obtaining assurance on the conditions of CAs associated with Jordan's Principle is unclear and reduces effectiveness and efficiency. This may lead to weaker external reporting, reputational damage for the initiative and the Department as well as limited information which may impact the provision of services that meet the needs of First Nations children.

Findings

Jordan's Principle relies on the reports submitted by recipients to collect data on types of products and services delivered, number of children served and the cost of products and services. During file testing, it was found that the reports submitted by recipients were incomplete and not consistent. It was also observed in several instances where reports were not submitted, or did not meet the minimum requirement of outlining the products and services provided and number of children served during the reporting. Furthermore, review and follow-up was conducted for recipient reporting on an as-needed basis due to limited capacity.

Monitoring of the intended outcomes and financial conditions of CAs was not documented and generally not carried out. Within the CAs, there were no defined monitoring requirements. Further, the audit team could not be provided with any evidence to demonstrate that formal monitoring was taking place within regions. Given the limited capacity of regions and the lack of guidance and expectations, any monitoring performed was done on an ad-hoc and informal basis based on a specific region's judgment and capacity.

While the draft SOP and MCF have outlined high-level expectations for monitoring of CAs, there are no specific requirements, guidance or expectations around the level and types of monitoring to be conducted by regions, as well as any thresholds/conditions to trigger monitoring. As such, there is not a formal, consistent and risk-based approach to monitoring across regions. To summarize, it was observed that there is inconsistency between the expectations established through the SOP and MCF, the terms and conditions of CAs and the existing practices for monitoring the use of group recipient funds through Jordan's Principle.

Recommendation

6. The Senior ADM of FNIHB should adopt a risk-based approach to the oversight of reporting and monitoring the external use of funds through Jordan's Principle.

6.2 Employees Involved with Jordan's Principle

Variation and Volume

Since the 2016 implementation of the Government's approach to Jordan's Principle, the Jordan's Principle team has been managing service delivery while developing business processes, protocols and controls to support the administration and delivery of Jordan's Principle. The implementation of Jordan's Principle is still relatively recent and is continuing to evolve with the development of guidance documents such as the SOP and MCF action plan.

The operational environment for Jordan's Principle is driven by a sense of urgency to ensure that requests are processed and decisions are made within the CHRT mandated timelines. The volume and variation of requests have generally increased the workload for regional Jordan's Principle teams and requires a breadth of knowledge as requests can be for health, social and educational needs.

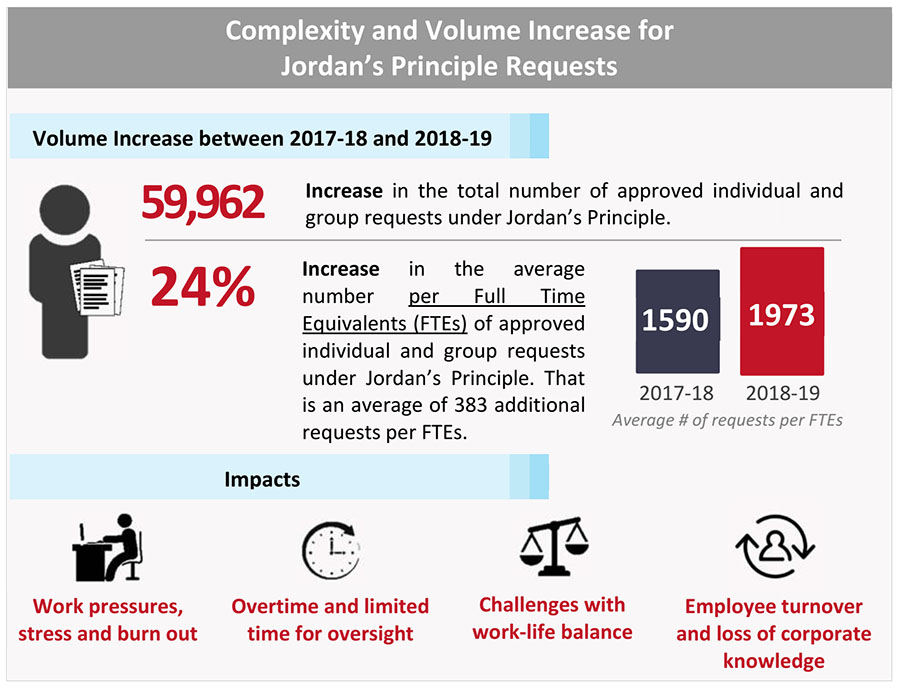

The commitment and dedication of the employees involved in Jordan's Principle to ensure that service delivery to First Nations children remains a priority has been an asset and important to the Department's implementation of the Principle. Based on their experience, they have a significant amount of corporate knowledge related to the Principle's history as well as the request files. Figure 3 provides a snapshot of the operating environment for regional Jordan's Principle teams.

Figure 3: Variation and Volume

Text alternative for Figure 3: Variation and Volume

Figure 3 illustrates the complexity and volume increase for Jordan’s Principle requests. It shows the volume increase between 2017-18 and 2018-19. During this period, there was an increase of 59,962 in the total number of approved individual and group requests under Jordan’s Principle. For 2017-18 the average number of requests per Full Time Equivalents (FTEs) was 1590 requests. For 2018-19 the average number of requests per FTEs was 1973 requests. These numbers represent a 24% increase in the average number per FTEs of approved individual and group requests under Jordan’s Principle. That is an average of 383 additional requests per FTEs. The increase in complexity and volume of requests under Jordan’s Principle has multiple impacts: Work pressures, stress and burn out; Overtime and limited time for oversight; Challenges with work-life balance; and, Employee turnover and loss of corporate knowledge.

Given the challenges and pressures in the operational environment, the audit expected to see that Jordan's Principle employees are provided with the tools and support necessary to fulfill their roles, responsibilities and accountabilities.

Risks

The tight timelines to make decisions, the variation of the requests, and the volume of the requests increase the emotional stress and demands on employees, which may result in employee turnover and loss of corporate knowledge. Additionally, due to the volume and tight timelines under which requests are processed, there is limited time for oversight of the review and approval process for Jordan's Principle requests.Findings

Jordan's Principle employees are working overtime in order to meet the mandated timelines and address the high number of requests. This results in stress and has impacted work-life balance as teams continue to provide essential services to First Nations children. At the FNIHB regional level, employees felt supported within their operational teams as regional level management have implemented informal measures such as teleworking, office quiet rooms, social activities and daily stand-up meetings where ideas are shared to help employees deal with the workload and stress.

Although steps have been taken to help employees cope with current stress of the operating environment of Jordan's Principle, in some interviews, employees noted that there were gaps in the support provided to them to help them deal with the increase in the volume and variation of Jordan's Principle requests.

The Department has drafted a Wellness Plan, which includes several initiatives to improve wellness, but has not yet been approved or implemented.

In order to support and streamline the work of employees, the Jordan's Principle team has developed the SOP, which provides policy background and clear direction to process requests for First Nations children under Jordan's Principle. The intended audience for the SOPs is Focal Points, Regional Executives, Regional and National Office Intake Officers, ADMs and any other decision maker in the process to evaluate requests or appeals under Jordan's Principle. Moreover, the Department's in-house Business Intelligence Unit is in the process of developing a case management tool (as part of the Synergy in Action initiative), which aims to reduce the administration burden and reduce employee workload.

Focal point employees used the escalation process if a request is recommended for denial on the basis of a concern with the recommended intervention, or to safeguard the best interest of the child. Employees adjudicating Jordan's Principle requests did not always receive feedback, rationale or lessons learned from Senior Management on their final decision when a request had been escalated for Senior ADM approval. The June 2019 revised SOP stated that regional Jordan's Principle focal point employees (CAs adjudicators) will be able to attend the Senior ADM Escalation Review meetings, which will allow employees to better understand the rationale for certain decisions that are made as part of the escalation process. The involvement will also allow employees to be more engaged to potentially reduce the number of requests that are escalated in the future.

Recommendation

7. The Senior ADM of FNIHB , in consultation with all involved sectors, should provide additional assistance to employees to better equip them to respond to the increase in volume and variation in the Jordan's Principle requests by finalizing and implementing the Wellness Plan and by providing global feedback and lessons learned throughout the adjudication process.

Internal Conflict of Interest

In phase 2 of the audit, processes and controls in place to address internal conflict of interest (COI) within the departmental context of Jordan's Principle were assessed. Processes and controls related to external COI were not reviewed.

The Jordan's Principle decision-making process is decentralized across regions, whereby regional employees (CAs focal points or delegated employee members) are responsible for the evaluation of requests and determination of approval or escalated for ADM review from communities and service providers. In some instances, these employees are either from the communities to which the Department provides services, are well-connected to communities due to their industry experience or work experience and/or are eligible to apply to Jordan's Principle. Therefore, the potential for instances of real or perceived COI while addressing Jordan's Principle files is high.

Risk

There is a risk that a real and/or perceived COI may exist due to the lack of defined parameters to inform decision-making on Jordan's Principle requests. In both cases, there could be an impact to the reputation of the initiative and the Department.

Findings

While there are departmental-wide processes and guidance (CAs values and ethics is a foundational element of being a public servant), there are no formal processes developed for COI in the context of administrating and delivering Jordan's Principle. The current SOP does not include any guidance, processes and expectations related to COI.

It was noted that FNIHB regional employees who were interviewed had a consistent understanding of how to identify and manage instances of COI. For example, employees understood that they cannot adjudicate a file if the requestor is from the same community, if the requestor is known to them or is a relative. Notwithstanding, these practices were not documented for Jordan's Principle and were done on an informal basis based on the discretion and judgment of the particular region.

At the moment, an honour system is being utilized where Senior Management trusts employees to be professional and ethical in the conduct of their work, as well as relying on the departmental-wide expectations for COI. The level of concern related to COI within the context of delivering and administrating Jordan's Principle was not high despite regions having faced instances of real and perceived COI, which were subsequently addressed.

The MCF action plan currently under development has outlined Management's expectations related to having "appropriate and confidential channels exist for disclosure of suspected improprieties or potential conflicts of interest".

Recommendation

8. The Senior ADM of FNIHB should formalize the existing internal conflict of interest practices specific to Jordan's Principle's operational context.

Internal Financial Wrongdoing

Internal financial wrongdoing refers to improper or illegal acts characterized by deceit, concealment or violation of trust committed by internal employees involved in the delivery and administration of programs. Examples of this can include misappropriation of funds, intentionally approving products and services that are ineligible, fictitious vendors or fraudulent invoicing and collusion.

The role of management with respect to preventing financial wrongdoing is the identify their financial wrongdoing risks and implement appropriate management controls to prevent them. The Department is currently undergoing a "Fraud Risk Assessment", with a focus on assessing the processes and controls in place to manage financial wrongdoing and fraud.

The role of Internal Audit is to evaluate the potential for the occurrence of fraud or financial wrongdoing and how the Department manages those risks. Given the ongoing fraud risk assessment being completed by management, the audit focused solely on examples of potential fraud conditions identified through file testing and during interviews.

Risk

There is a risk that Jordan's Principle funds may be misappropriated due to a lack of appropriate and effective oversight controls. Likewise, instances of internal financial wrongdoing may not be detected within the conduct of operational activities. This risk is further driven by the increasing pressures related to reviewing and approving requests (e.g. volume, timelines, and lack of defined parameters).

Findings

Currently, there is limited documentation that outlines or communicates roles and responsibilities, and expectations for the identification and management of wrongdoing related to Jordan's Principle. There are a limited number of defined processes in place for the reporting and escalation of internal financial wrongdoing issues and/or concerns.

File testing during both phases of the audit demonstrated that there was a lack of documentation or information to be able to trace changes in approved funding. Proposals and intake forms were not consistently used, which made it difficult to trace amounts within CAs amendments or Notice of Budget Adjustments in certain instances. This is consistent with the audit team's findings in phase 1, which noted that files did not always include sufficient or complete information to support decisions of approval for additional funding.

While several service standards for fraud detection exist within the MCF and SOP (e.g. development and communication of fraud scenarios, fraud identification, fraud reporting, corrective/mitigate actions), fraud management guidance and strategies were not found to be documented or specifically addressed within the MCF action items.

Similar to the observation related to COI, Senior Management relies on employees to be professional and ethical in the conduct of their work and rely on the departmental-wide expectations for wrongdoing (CAs roles and responsibilities of being a public servant and sign off as part of their Government of Canada employment agreement). While this contributes to the mitigation of the risk of fraud or financial wrongdoing, it is not sufficient on its own.

Recommendation

See recommendation 2. The post-decision review of file completeness will also confirm that approved funding requests are explained and documented with supporting evidence in the file.

6.3 Raising Awareness with Canadians

Given that the CHRT Orders were released in 2016, the implementation of Jordan's Principle is relatively new for the Department and for Canadians. There may be a perception that Canadians may misunderstand how Jordan's Principle is using federal funds to support to First Nations children education, social and health needs.

There is a risk that it will be more difficult for the Department to achieve its goal to support substantive equality for education, social and health needs for First Nations children if Canadians misunderstand the importance of Jordan's Principle. The Department used multiple methods to provide information about Jordan's Principle. The Department used various social media websites, a First Nations newspaper, Weather Network and mobile advertising (e.g. Youtube, Facebook, Twitter and LinkedIn, First Nations Drum, Pelmorex and Native Touch) to provide information targeting groups such as First Nations families and foster parents as well as education, social development and health professional in both First Nations communities and in urban settings. This information focussed on providing awareness of Jordan's Principle, encouraging parents and guardians to access Jordan's Principle as needed and encouraging professionals to share information about Jordan's Principle with families. The Department also used its departmental website to provide information more broadly. The information included the definition of Jordan's Principle, the number of approved Jordan's Principle requests to date, the definition of substantive equality and information on the type of services provided by the Principle as well as how to access them (e.g. eligibility criteria, contacts per region, submitting a request and seeking reimbursement). While there have been efforts to increase the awareness of Jordan's Principle and how it can be accessed, there remains an opportunity to build awareness more broadly of the results achieved by Jordan's Principle and their importance. 9. The Senior ADM of FNIHB , in consultation with Communications, should work towards developing and implementing a communication strategy to directly target the wider population to build awareness of the importance of Jordan's Principle. Risk

Findings

Recommendation

7. Conclusion

A unique challenge with Jordan's Principle has been the need to develop business processes while managing and delivering the Principle under tight deadlines and high pressure. Jordan's Principle is a unique initiative; therefore, a pre-existing model for its implementation is not available. In addition, a traditional period of design for the initiative is not available due to high demand and time constraints which resulted from implementation of the CHRT orders. Due to the changing landscape under which the Principle operates, the business processes and the definition and scope of what is required under Jordan's Principle have been continuously adapted to the CHRT orders.

In phase 1, the audit found that the Department has positioned itself to fully manage some of its risks related to the availability of information, communications with First Nations as well as financial practices including delegation of authority, Financial Administration Act (FAA) Section 34 and 33, and quality assurance reviews for payments. The employees and the follow-up they perform have helped the Department partially mitigate some of its information and knowledge risks.

In phase 2, the audit found that the Department had positioned itself to partially mitigate some of its risks related to the coordination and collaboration between all sectors involved in Jordan's Principle, identifying opportunities to address commonly occurring needs of First Nations children, ensuring that employees are equipped to respond to the variation and volume of Jordan's Principle requests, real and perceived conflicts of interest and building awareness of the importance of Jordan's Principle to all Canadians. The Department has not fully implemented the mitigation measures that they identified to oversee the monitoring and reporting requirements in the contribution agreements.

The audit team identified recommendations to address the remaining risks to the Department.

Recommendations

- Going forward, the ADM of FNIHB should ensure that information stored in multiple locations is consolidated into the request file. This will allow information to be found more easily in the future.

- While there is a strong sense of urgency to make a decision within the timelines mandated by the CHRT, the timelines stop once the decision is communicated. The Senior ADM of FNIHB should ensure that a post-decision review of file completeness is performed to ensure that information required by management in the Standard Operating Procedures is present and accessible for future reference.

- The Senior ADM of FNIHB , with support from the CFRDO, should implement a monitoring process to ensure that FAA Section 32 commitments are being input into SAP after the decision has been communicated and that unused funds are released after final payment. The results of the monitoring should be addressed through corrective action as required.

- The Senior ADM of FNIHB in consultation with ESDPP, CFRDO, CFSR and RO should formally define and communicate roles, responsibilities and accountabilities for all sectors involved to ensure efficient coordination of their approach to implementing Jordan's Principle.

- The Senior ADM of FNIHB should leverage data trends to proactively identify alternative ways to provide commonly requested products and services through existing or new programs.

- The Senior ADM of FNIHB should adopt a risk-based approach to the oversight of reporting and monitoring the external use of funds through Jordan's Principle.

- The Senior ADM of FNIHB , in consultation with all involved sectors, should provide additional assistance to employees to better equip them to respond to the increase in volume and variation in Jordan's Principle requests by finalizing and implementing the Wellness Plan and by providing global feedback and lessons learned throughout the adjudication process.

- The Senior ADM of FNIHB should formalize the existing internal conflict of interest practices specific to Jordan's Principle's operational context.

- The Senior ADM of FNIHB , in consultation with Communications, should work towards developing and implementing a communication strategy to directly target the wider population to build awareness of the importance of Jordan's Principle.

8. Management Action Plan

| Recommendations | Management Response / Actions | Responsible Manager (Title) | Planned Implementation Date |

|---|---|---|---|

| 1. Going forward, the Senior Assistant Deputy Minister (ADM) of FNIHB should ensure that information stored in multiple locations is consolidated into the request file. This will allow information to be found more easily in the future. | Management agrees with the recommendation. For the paper files, a 'Checklist', of the required documentation to be maintained, with each request file, will be developed and provided to all regions. The SOPs will also be updated to reflect this requirement. Synergy in Action is developing a new case management system for Jordan's Principle with built-in quality assurance mechanisms to ensure that all mandatory documents are scanned and attached to the electronic file before completion. |

||

Key Deliverables:

|

Executive Director, Jordan's Principle | December 2019 | |

|

Executive Director, Jordan's Principle | March 2020 | |

|

Director, Synergy in Action | January 2020 | |

|

Executive Director, Jordan's Principle | April 2020 | |

| 2. While there is a strong sense of urgency to make a decision within the timelines mandated by the CHRT, the timelines stop once the decision is communicated. The Senior ADM of FNIHB should ensure that a post-decision review of file completeness is performed to ensure that information required by management in the Standard Operating Procedures (SOP) is present and accessible for future reference. | Management agrees with the recommendation. Jordan's Principle to develop and implement a quality assurance process for individual and group requests. In addition, the new case management system is being designed to incorporate quality assurance capabilities (e.g. timestamped audit trails when files are updated). |

||

Key Deliverables:

|

Executive Director, Jordan's Principle | May 2020 | |

| 3. The Senior ADM of FNIHB , with support from the CFRDO, should implement a monitoring process to ensure that FAA Section 32 commitments are being input into System Application Products (SAP) after the decision has been communicated and that unused funds are released after final payment. The results of the monitoring should be addressed through corrective action as required. | Management agrees with the recommendation. The requirement that Section 32 be completed by authorized personnel immediately following the approval of an individual request will be standardized in the new Child Request Form (Intake Form) for Jordan's Principle. This includes the requirement that the commitment is entered into SAP. In addition, Phase 1 of the new case management system will make the commitment number a mandatory field, ensuring that this step must be completed prior to continuing to the next step. Jordan's Principle, with support from CFRDO/BSFO, will develop and communicate a common process for the ongoing monitoring and management of commitments ensuring that unused/unclaimed funds are released on a timely basis. |

||

Key Deliverables:

|

Executive Director, Jordan's Principle | November 2019 | |

|

Executive Director, Jordan's Principle (co-lead) |

April 2020 | |

| 4. The Senior ADM of FNIHB in consultation with ESDPP, CFRDO, CFSR and RO should formally define and communicate roles, responsibilities and accountabilities for all sectors involved to ensure efficient coordination of their approach to implementing Jordan's Principle. | Management agrees with the recommendation. Jordan's Principle in collaboration with CIAD will engage with ESDPP, CFRDO, CFSR, and RO to formally define roles, responsibilities and accountabilities for all sectors involved to ensure efficient coordination of their approach to implementing Jordan's Principle. These will be documented in SOPs as well as the FNIHB SADM approved Terms of Reference of the Jordan's Principle and Inuit CFI Management Committee. In addition, the Jordan's Principle and Inuit CFI Management Committee currently meets on a monthly basis and is mandated to provide clear and consistent operational direction on the departmental administration of Jordan's Principle and Inuit CFI. Membership of the committee includes ESDPP, CFRDO, CFSR and RO. |

||

Key Deliverables:

|

Executive Director, Jordan's Principle (co-lead) |

March 2020 | |

|

Executive Director, CIAD | April 2020 | |

| 5. The Senior ADM of FNIHB should leverage data trends to proactively identify alternative ways to provide commonly requested products and services through existing or new programs. | Management agrees with the recommendation. FNIHB is committed to tracking the type of products, supports and services being approved for funding under Jordan's Principle through various systems such as the new case management system, SAP, and GCIMS. Data trends will be used going forward to identify gaps that could be addressed through existing or new programs. FNIHB is also committed to continuing to engage regularly with provinces and territories, as well as the Assembly of First Nations and Service Coordination Organizations to leverage data holdings of service coordinators and communities for analysis. |

||

Key Deliverables:

|

Executive Director, Jordan's Principle | April 2020 | |

|

Executive Director, Jordan's Principle | April 2021 | |

|

Executive Director, Jordan's Principle (co-lead) Director – SHIPCU, SPPI (co-lead) |

September 2020 | |

|

Executive Director, Jordan's Principle | September 2021 | |

| 6. The Senior ADM of FNIHB should adopt a risk-based approach to the oversight of reporting and monitoring the external use of funds through Jordan's Principle. | Management agrees with the recommendation. FNIHB is in the process of reviewing the most current risk profile for Jordan's Principle (updated in Fall 2019) and developing a risk-informed approach for reporting and monitoring. Jordan's Principle and CIAD are committed to enforcing the existing procedures for the reporting management of funding arrangements in the regions. CIAD in collaboration with Jordan's Principle will develop a communication to the regions enforcing the adherence to the reporting monitoring procedures. |

||

Key Deliverables:

|

Executive Director, Jordan's Principle (co-lead) | December 2019 | |

|

Executive Director, CIAD (co-lead) | November 2019 | |

|

Executive Director, CIAD (co-lead) Executive Director, Jordan's Principle (co-lead) |

November 2019 | |

|

Executive Director, Jordan's Principle (co-lead) |

April 2020 | |

| 7. The Senior ADM of FNIHB , in consultation with all involved sectors, should provide additional assistance to employees to better equip them to respond to the increase in volume and variation in Jordan's Principle requests by finalizing and implementing the Wellness Plan and by providing global feedback and lessons learned throughout the adjudication process. | Management agrees with the recommendation. Jordan's Principle will finalize the wellness plan through approval by the Jordan's Principle and Inuit CFI Management Committee. Ongoing oversight and monitoring of the wellness plan will be conducted through the Jordan's Principle and Inuit CFI Management Committee. The new case management system will better equip employees with a more standardized and consistent process, and a live dashboard showcasing employee workload. |

||

Key Deliverables:

|

Wellness Lead, FNIHB (co-lead) |

October 2019 | |

| 8. The Senior ADM of FNIHB should formalize the existing internal conflict of interest practices specific to Jordan's Principle's operational context. | Management agrees with the recommendation. Jordan's Principle is developing mechanisms to formalize internal conflict of interest practices for Jordan's Principle and including them in the Standard Operating Procedures (SOPs). Jordan's Principle, in collaboration with the regions, will incorporate training on the internal conflict of interest process. |

||

Key Deliverables:

|

Executive Director, Jordan's Principle | December 2019 | |

|

Executive Director, Jordan's Principle | January 2020 | |