Management Action Plan Workbook

Table of contents

- 1. Purpose of Management Action Plan Workbook

- 2. Why a MAP?

- 3. Recipient - Appointed Advisor

- 4. Steps in Completing a Management Action Plan

- 5. Instructions and Forms for Recipients to Complete a Management Action Plan

- Annex A: MAP Form A: Action Plan – Completed Example

- Annex B: MAP Form B: Financial Plan – Completed Example

- Annex C: MAP Form C: Capacity Development Plan – Completed Example

- Annex D: Criteria for MAP Evaluation

1. Purpose of Management Action Plan Workbook

The Management Action Plan (MAP) Workbook was developed to assist recipients who are required to prepare a MAP. Departmental staff responsible to review a MAP submitted by a recipient should refer to this workbook for guidance.

The MAP Workbook is not intended to constitute advice, recommendations or direction to the recipient from the department(s) on how they should manage their own affairs.

Completed examples of Form A: Action Plan, Form B: Financial Plan and Form C: Capacity Development Plan can be found in Annex A, B and C respectively.

Definitions for terms used throughout this workbook are contained in the Default Prevention and Management Policy.

2. Why a MAP?

Through the 'Default Assessment' process, the department(s) may identify that a recipient is in default of its funding agreement. The funding agreement allows the department(s) to require that the recipient develop and implement a MAP that is acceptable to the department(s) within 60 calendar days from the day the default notice is given to the recipient.

A default is as specified in the funding agreement and may include:

- the recipient defaults in any of its obligations set out in the current funding agreement, a prior agreement, or in any other agreement through which a federal department funds the recipient;

- the auditor of the recipient gives a disclaimer of opinion or adverse opinion on the financial statements of the recipient in the course of conducting an audit pursuant to a funding agreement;

- in the opinion of the department(s), with regards to any financial information relating to the recipient and reviewed by the department(s), the financial position of the recipient is such that the delivery of any Program for which funding is provided under the funding agreement is at risk;

- in the opinion of the department(s), the health, safety or welfare of the service population is at risk of being compromised; or

- in the case of an incorporated recipient, the recipient becomes bankrupt or insolvent, goes into receivership, takes the benefit of any statute from time to time being in force relating to bankrupt or insolvent debtors, or ceases to be in good standing with whichever federal or provincial jurisdiction in which the recipient was incorporated.

In this context, a low risk default situation should generally be resolved within 90 days.

A medium risk default may take longer to resolve and require more substantial resources (as outlined in the MAP).

The recipient is responsible to address its default(s). For the MAP to be acceptable to the department(s), it will need to convey the strategy that the recipient will use to address their default. The MAP will need to set out:

- the default(s) to be resolved as identified in the department(s') notice to the recipient of the requirement to prepare and implement a MAP;

- a comprehensive resolution strategy;

- the necessary actions required to implement the strategy; and

- the operating timeframe / timelines, i.e. effective date, review dates, completion date and termination date.

The extent of the MAP should reflect the complexity of the default(s) identified by the department(s), yet contain all of the above elements.

3. Recipient-Appointed Advisor

If the recipient determines that they need advisory services or if the department(s) requires the recipient to seek such support to assist them in resolving the default, the MAP should outline the expected deliverables of the recipient-appointed advisor, time lines and performance measures that would allow for the MAP's completion.

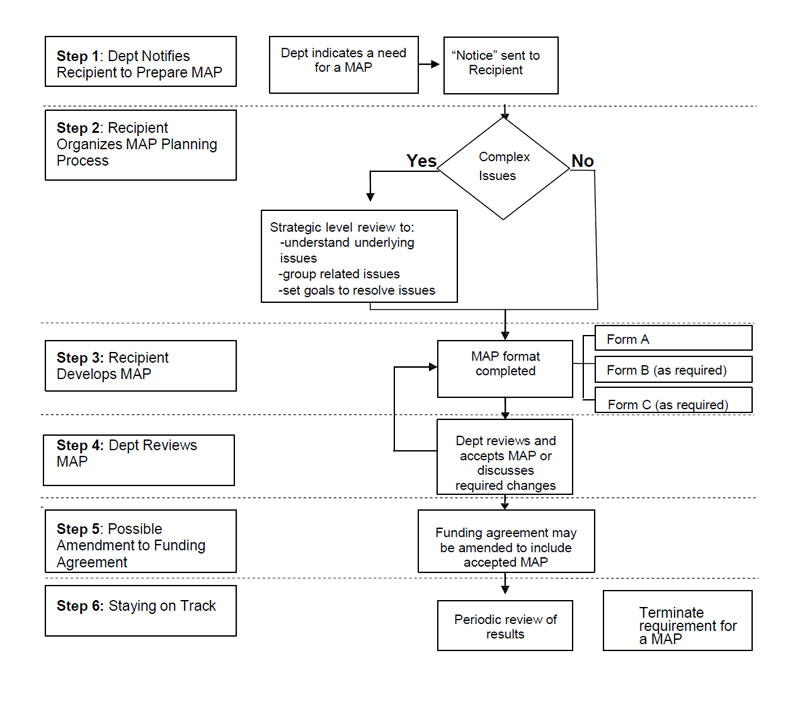

4. Steps in Completing a Management Action Plan

Text description of Figure 1: Steps in Completing a Management Action Plan

Step 1: The department(s) Notifies Recipient to Prepare MAP

- The department(s) identifies one or more default(s).

- The department(s) notifies the recipient of the identified default(s), the requirement for a MAP to be developed and implemented, and an invitation for the recipient to communicate to the department(s), within a specified time frame, as well as the recipient's view as to whether there are any factual errors in the notice.

Step 2: Recipient Organizes MAP Planning Process

- The recipient should begin to establish a work plan and project team.

- The recipient's Senior Administrative Officer may be well positioned to manage the project with oversight from a representative or member of the recipient's management team. Key staff or advisors with knowledge and expertise of the subject matter should be brought into the team. A recipient-appointed advisor may be sought.

Step 3: Developing a Detailed Project Plan

- The standard MAP includes up to three parts:

- Form A – Action Plan – to be completed in every case

- Form B – Financial Management Plan – to be completed where the notice of the requirement to prepare and implement a MAP identifies financial health issues or where financial health issues are evident

- Form C – Capacity Development – to be completed where capacity development will be needed to address immediate concerns and/or to support long-term sustainability and success of the organization

Step 4: Department(s') Review of the Plan

- Annex D includes a checklist used by the department(s) to assist in assessing whether the MAP is acceptable. The recipient may wish to use this checklist to help make its own determination as to whether the MAP is complete.

- In other words, the MAP should contain a detailed plan with corrective actions and steps for implementation and conclusion to address the default(s).

Step 5: Amendment to the Funding Agreement

- When a finalized MAP is acceptable to the department(s), the department(s) will invite the recipient to amend the funding agreement to incorporate the MAP.

- This amendment will set out a process for reporting on progress of the MAP and for ongoing review of the results.

Step 6: Staying on Track

- The department(s) will review the MAP as often as is deemed necessary given the nature and extent of the default situation. This review may determine that:

- The MAP is progressing as expected and no changes to the MAP are required;

- The MAP is progressing as expected but changes to the MAP that are proposed by the recipient or deemed necessary by the department(s) may be required, given changing circumstances or to improve performance;

- The MAP is not progressing as expected and a reassessment of the situation is required; or

- The MAP has achieved the required results and the requirement for the MAP can be terminated.

- The department(s) makes an assessment of whether a requirement for a MAP will be terminated. The following criteria will be used by the department(s) when considering the termination of a MAP:

- High and medium priority items in Form A: Action Plan have been met;

- The recipient has a plan of action for resolving lower priority issues (department(s) may devise an ongoing monitoring plan of these outstanding items); and

- The recipient has plans to continue with capacity development, as required, to avoid recurrence of these problems.

5. Instructions and Forms for Recipients to Complete a Management Action Plan

5.1 Structure of the MAP

A Management Action Plan (MAP) acceptable to the department(s) will consist of up to three forms as follows:

- Form A: Action Plan: is required where the recipient has, for example, not employed qualified staff (e.g. certified teachers), where required by the funding agreement

- Form B: Financial Plan: is required where the recipient must improve its financial position

- Form C: Capacity Development Plan: is required where the recipient needs specific capacity building activities

Form A – Action Plan is required in every case. Forms B and C are prepared as required.

5.2 MAP Forms

Management Action Plan Form A - Action Plan

Form A details the potential cause of the default and the corrective measures that will be taken to resolve them. Form A may be used to present both the strategic and project level plans.

Documentation Guidelines

- Deal only with goals and objectives specific to that group of default issues raised;

- Use point form, bullets and numbering;

- Refer to activities set out in Form B and Form C as applicable; and

- Complete the form in the following sequence:

- Problem Identification

- Global Goals

- Goal Priorities

- Global Performance Measures

- Objectives

- Tasks

- Persons Assigned

- Timeline

- Documents/Milestones

- Review Frequency

For simplicity and coherence, the Action Plan may be organized in accordance with the "risk factors/considerations" found in the General Assessment (GA).

A MAP may be used to resolve "simple" or "complex" issues. A "simple" issue is one where the action required to correct is clear whereas a "complex" issue may involve a situation whose underlying causes are not clear nor are the actions required to correct them.

A detailed project planning process may be needed to fully address complex situations. The recipient may wish to arrange a strategic level discussion before such detailed planning begins. Such a discussion could:

- build a better understanding of the issues;

- group similar issues into manageable pieces for resolution (e.g. governance, finance, social program); and

- set global goals to guide the project.

The recipient may desire to have this process go beyond the defaults to their underlying causes with the aim of building capacity and minimizing the likelihood of the problem reoccurring.

To be acceptable to the department(s), the first part of Form A must include an outline of the high level issues identified as the cause of the default(s), the goals, the performance measures and the resources to be put in place by the recipient to address these issues.

Before a series of action plans are devised to address the default, an informal information gathering session may take place to help to identify the underlying root causes, the outcomes to be achieved (that will need to be addressed by the action plan), and performance measures that demonstrate that the action plan will be successful.

Problem Identification and Understanding

The "Problem Identification" statements are based upon the notice from the department(s), outlining the issue(s) identified and requiring preparation of the MAP to correct these defaults. The MAP must respond clearly to the requirements of the notice.

A facilitated brainstorming session may be best where the issue is complex and requires some analysis to understand the underlying problems. The recipient may wish to keep this working group small so the process will not become cumbersome.

Problems identification statements should be based on verifiable facts or indicators and not personal opinion. Some sources of information that can be drawn upon to best determine the underlying issues are:

- Input from departmental offices;

- Auditor; and

- Elders, managers, employees and band members.

The brainstorming session may involve representatives from any or all of these areas and may also be extended to discuss the high level/global goals in addressing these issues.

High Level Goals

The "global" or high level goals should relate directly to addressing the identified issues observed in the "Problem Identification" portion of Form A. The recipient may want to consider that; goals and their supporting objectives, tasks, time lines, persons assigned and milestones follow SMART guidelines:

- Specific

- Measurable

- Achievable

- Relevant/Reviewable

- Timely

Each goal should be related to at least one of the problems identified.

Figure 2: Characteristics of "S.M.A.R.T" Goals

- Specific: Specific goals have a much greater likelihood of being achieved than do goals that are too general. A two stage planning process (strategic to project) allows progressing from more general to more specific goals.

- Measurable: Measurable goals are observable and tenable. They also allow the project team to report on progress to the recipient (i.e. governing authority) and then to the department(s).

- Attainable: Attainable goals are realistic and the organization is willing and able to implement them. They may be challenging and require commitment to attain.

- Relevant: Achieving the goal will fix the specific problem being addressed or achieve the result being sought.

- Timely: Goals should be set in logical order with attention given to priorities and those tasks that must be completed before others can start. Each task is given a start and end date and fixed duration.

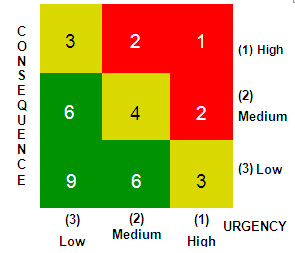

Priority Setting

The recipient may wish to rate the issues and corresponding goals to address these issues as a low, medium or high priority. In order to determine the priority, the urgency and the consequences of each issue should be reviewed.

Priority = Urgency x Consequence

Where:

Urgency = how quickly the problem needs to be resolved

Consequence = how adverse is the effect of the problem on the service population.

The recipient may wish to use the following scales to determine the level of urgency and consequence:

| High | The potential negative impacts could not be reversed by their very nature (e.g. loss of life or suffering) or due to the cost of rebuilding assets. |

|---|---|

| Medium | The potential negative impacts can be remedied, but there are impacts to the wellbeing of individuals and the achievement of longer term objectives. |

| Low | Action is required but can be delayed until higher priority items are addressed. |

| High | Programs are disrupted threatening the health & safety of the service population or essential community infrastructure. Minimal member support for Administration and Chief and Council. |

|---|---|

| Medium | Programs are disrupted creating hardship for the service population. Moderate support for Administration and Chief and Council. |

| Low | Programs are delivered with minimal impact, health and safety is not impaired. High level of support for Chief and Council and Administration. |

- Red zone items are high risk and must be given the highest priority.

- Yellow zone items are medium risk and action may be delayed.

- Green zone items are low risk covered in longer term plans.

Performance Measures

Performance Measures help gauge the progress of the MAP and determine whether or not the action plan is successful.

Performance measures are verifiable indicators or proof that the goal is being achieved. Performance measures are determined at the high/global level and at the task level. Both are determined at the outset of the MAP in order to review progress as the plan is executed. It should be possible to match qualitative or quantitative performance indicators to high level problems and goals, or the goals should be re-examined.

Performance measurements meet the following criteria:

- Relevant – the indicator provides evidence that can be directly or indirectly influenced by the action plan

- Reliable – the indicator can be used by different people with consistent results

- Valid – the indicator is based on identifiable criteria that measure what they are intended to measure

- Credible – the indicator is trustworthy

- Consistently measurable over time – it is necessary to demonstrate that progress is made and targets are achieved over time

- Detailed – the indicator is in detail that can be sufficiently monitored and connected to the action plan

- Designed to separate the monitor and monitored – minimize conflicts of interest when an actor monitors its own performance

- Available – existing data can be used to construct the indicator, or current processes and reporting can be amended to accommodate required data

Overall, quality of performance measurement indicators should be a higher priority than quantity. The frequency of collection and reporting should be considered, as well as the capacity required to implement these performance measures.

Task Level

After identifying the issues and what the MAP should achieve at a high level, the MAP needs to define the detailed action plan that will allow for the achievement of these high level goals and to address the default in a sustainable manner. This section in Form A includes:

- The objective of each action plan and what it is meant to achieve, as well as a list of specific tasks that will achieve these detailed objectives.

- A time line for the achievement of the objective.

- The person(s) assigned to and/or responsible to ensure completion of each given task.

- Performance measures that will demonstrate that the task has been completed as well as the frequency that the recipient will review the progress of the task.

Objectives

Objectives relate to specific activities required to attain the global goals. By completing these tasks, the objective should be achieved and hence progress made towards the higher level global goals. Each objective should be related to/aligned with at least one of the global goals at a strategic level and noted in the description of the objective.

Each objective is assigned a priority based upon the global priority goal to which it relates. For instance, if one objective relates to a global goal that is low and another that is high priority, it would be deemed a high priority objective. High priorities should be given attention over low and medium priority objectives.

Task / Timeline / Person(s) Assigned

Be specific about the task that is to be completed so that proper performance measurements can be put into place to determine the progress of the task.

Tasks should relate directly to achieving the objectives and should list only major activities that need to be conducted in order to meet those objectives. A target start date and completion date are specified, which allows the reviewer to determine whether the task has been completed according to schedule or whether there have been overruns. A person with appropriate knowledge/skills should be assigned to each task. This could be someone internal to the organization and/or may also require the aid of a recipient-appointed advisor.

Especially where a recipient-appointed advisor is required, it is important to be very clear about the timing of the tasks and responsibilities of the resource so that these can be monitored. These expectations should be embedded in the contract between the recipient and the recipient-appointed advisor.

Results / Performance Measures

The guidelines for creating global performance measures are the same as to those pertaining to the individual tasks: relevant, reliable, valid, credible, consistently measurable over time, detailed, designed to separate the monitor and the monitored, and available. At the project level, however, the performance measures should describe the specific measurements of the task being performed. This could be quantitative (number of…) or qualitative (description of state of being), but must be measurable in order to demonstrate that the action has been completed and has been completed successfully in line with the objectives. It must also determine how the activity or milestone can be structured to provide a specific performance measure that will allow the monitoring of progress.

Performance reporting should be well documented. Where multiple milestones and performance measures are available, preference is given to those which use concrete statistics or have binary outcomes.

Output indicators – measure tangibles or products that are measured in units (e.g. number of...)

Outcome indicators – reflect progress toward a desired end state of the target group (e.g. operating capacity to deliver services….)

Review Cycle (by the Project Team or Recipient)

The internal review cycle set for a MAP should be based upon:

- How important completing a task is to the completion of the larger project (i.e. tasks that have to be completed before others proceed);

- The risk associated with a task (completion of some tasks is more uncertain than others and they may be subject to more frequent review); and

- The need to link it to the department(s’) review schedule (generally quarterly reviews but more frequent reviews may be necessary to manage risk).

Form A (Mandatory): Action Plan

| Problem Identification (Group of Issues #1) | Global Goal(s) | Global Performance Measures |

|---|---|---|

| Problem #1 Risk Rating (Low/ Medium/ High) |

Goal #1 Related Problems(s): |

|

| Problem #2 Risk Rating (Low/ Medium/ High) |

Goal #2 Related Problems(s): Goal Priority (Low/ Medium/ High) |

|

| Goal #1 Related Problems(s): |

Goal #.... |

| Objective | Task/subtasks | Time Line | Person(s) Assigned | Results/ Performance Measure |

Review Frequency |

|---|---|---|---|---|---|

| Related Goal(s) Objective Priority ((Low/ Medium/ High) |

|||||

| Related Goal(s) Objective Priority ((Low/ Medium/ High) |

|||||

| Related Goal(s) Objective Priority ((Low/ Medium/ High) |

| Problem Identification (Group of Issues #...) | Global Goal(s) | Global Performance Measures |

|---|---|---|

| Objective | Task/subtasks | Time Line | Person(s) Assigned | Results/ Performance Measure |

Review Frequency |

|---|---|---|---|---|---|

Management Action Plan Form B – Financial Plan

Form B: Financial Plan is completed where the recipient must improve a financial risk situation (e.g. to deal with a debt situation). It requires that future financial projections be prepared.

Form B: Financial Plan requires an assessment of current expenditure patterns and a discussion of how revenues may be increased and/or expenditures controlled in order to balance the budget. A schedule of payables may be required to manage repayment of debt. The past year audited consolidated financial statements should appear on Form B, as a point of reference. The results of the financial planning exercise sets out forecasted returns and planned expenditures for the current and future fiscal years.

| Budget Categories | Past Year | Current Year |

Current Year +1 |

Current Year +2 |

Current Year +3 |

|---|---|---|---|---|---|

| Program Revenues | |||||

| Total | |||||

| Program Expenditures | |||||

| Total | |||||

| Total Surplus / Deficit at Year-end | |||||

| Use of Surplus | |||||

| Loan Repayments Account | |||||

| Payable Arrears Deficit | |||||

| Reduction reduction | |||||

| Surplus (Deficit) at Year End |

| Payee | Amount | Disposition |

|---|---|---|

Management Action Plan Form C - Capacity Development Plan

Form C: Capacity Development Plan focuses on capacity building in order to prevent the default(s) and related issues from recurring. Form A may identify, for example, at the strategic level, a need for capacity development for elected officials and staff. Form C can be used to set out such a plan (e.g. training on strategic planning) or to correct a default situation (e.g. to hire certified teachers).

Form C should identify any capacity issues that may keep the recipient from delivering the services as contracted in the funding agreement. These may include the areas of financial concerns and governance. A plan should allow further capacity building activities.

Form C (Capacity Development Plan): is used to list specific actions that the recipient may take to correct defaults. For example, to hire qualified staff (e.g. certified teachers); or secure training for officials to complete a specific task.

There may be other documents that outline the recipient’s overall capacity development needs. For instance, the recipient may already have a Capacity Development Plan that addresses some capacity concerns that are contributing to the identified issues and defaults outlined in the MAP.

With respect to governance and capacity planning, the department(s) offers the Governance Capacity Planning Tool, which allows the user to identify areas of governance and capacity concerns in line with best practices.

Documentation Guidelines

Form C consolidates and highlights the capacity development component of the MAP. It may address specific defaults (e.g. need to employ certified teachers), or measures to help resolve defaults (e.g. training in strategic planning). Use bullets and numbering and complete the document in the following sequence:

- Key Position

- Training/Staffing Activity

- Desired Outcome (Objective per Form A)

- Training/Service Provider

- Responsible Person and Target Date

- Estimated Costs

| Key Position |

Training/Staffing Activity |

Desired Outcome |

Training / Service Provider |

Responsible Person & Target Date |

Estimated Costs |

|---|---|---|---|---|---|

Key Position

Provide name of any new position required or vacant position to be filled, or the individual(s) requiring training.

Capacity Activity / Training

Provide a description of course or other capacity building activity. Where this activity involves training, discuss how workload will be managed over the training period.

Desired Outcome (in Support of Objectives per Form A)

Asks: Which objective (as described in Form A) is this action going to help resolve? A linking statement is made between the capacity development action plan, and the defaulted item/objective in Form A.

Service Provider

Asks: How is the recipient going to procure this activity? / How is the recipient going to find someone qualified to fill this vacancy? Provide the name of the organization to provide the service. If this involves training a staff member, on-the-job support may be noted.

Responsible Person and Target Date

Asks: Who is overseeing and coordinating the capacity development activity? What is the target date of this procurement? Persons with appropriate knowledge/skill should be assigned to each task. Target start and completion dates need to be specified.

Estimated Cost

Asks: What is the expected cost of this activity/position/training over the course of a year? How much is training going to cost the recipient for every staff trained?

Annex A: MAP Form A: Action Plan – Completed Example

| FINANCIAL MANAGEMENT - Problem Identification | Global Financial Goal(s) | Global Performance Measures |

|---|---|---|

|

|

|

| Objective | Task/subtasks | Time Line | Person(s) Assigned | Results/ Performance Measure |

Review Frequency |

|---|---|---|---|---|---|

| Establish a Finance Committee consisting of the financial controller,

band manager and 2 council members

to sign cheques and approve all financial transactions Related Goal(s): 2,3 Objective Priority: High |

|

Immediately Completion by 07/15/2013 |

Band Manager in conjunction with Chief & Council | Terms of reference available for review Confirmation from the bank of new signing authorities. |

Review of Terms of reference by the Funding Services Officer 07/01/2013 |

| Establish a comprehensive budget which provides for repayment of

creditors and recovery of deficit as per

Form B. Related Goal(s): 1 Objective Priority: High |

|

Commencing 07/01/2013 Target 07/30/2013 |

Financial Management Board members | Comprehensive budget spreadsheet completed which conforms to reductions in Form B | Initial Review of budget by Funding Services Officer by 08/15/2013 Quarterly review with Audited Consolidated Financial Statements by Funding Services Officer |

| Bank Reconciliation completed monthly. Related Goal(s): 2 Resultant Priority: High |

|

Commencing 00/01/2013 |

Finance Clerk Financial Controller Finance Clerk |

Reconciliation completed and available for review within 7 days of receipt of bank statement 90% of the time. |

Monthly by the Financial Management

Board. Quarterly by Funding Services Officer |

| Establish a comprehensive budget process which ensures no unapproved over expenditures. > Related Goal(s): 3 Objective Priority: Low |

|

Commencing by 07/01/2013 Target 09/15/2013 Target 11/15/2013 |

Auditor Financial Controller |

Financial control framework completed and available for review by the department(s) and Creditors by established target date. | Internal review of framework by

10/15/2013 Review by the department(s) by 11/15/2013 |

| Establish a Financial Bylaw passed by the membership. Related Goal(s): 3 Objective Priority: Low |

|

Commencing 02/15/2014 Target 19/15/2014 Target 10/30/2014 Target 02/15/2014 |

Financial Management Board | Draft Financial code available for review by established due date Approval by membership by target date | Ongoing status updates |

Annex B: MAP Form B: Financial Plan – Completed Example

| Budget Categories | Past Year | Current Year | Current Year +1 | Current Year +2 | Current Year +3 |

|---|---|---|---|---|---|

| Program Revenues | |||||

| Economic Development | 75,000 | 100,000 | 125,000 | 127,500 | 130,050 |

| Social Development | 775,000 | 800,000 | 1,190,000 | 1,213,800 | 1,238,076 |

| Capital and Housing | 1,000,000 | 1,100,000 | 1,500,000 | 1,530,000 | 1,560,600 |

| Band Administration | 1,090,000 | 1,275,000 | 1,475,000 | 1,504,500 | 1,534,590 |

| Health | 475,000 | 600,000 | 773,000 | 788,460 | 804,229 |

| Education | 1,800,000 | 2,000,000 | 2,800,000 | 2,856,000 | 2,913,120 |

| Trust Funds | 0 | 0 | 0 | 0 | 0 |

| Other – Specify | 0 | 0 | 0 | 0 | 0 |

| Other – Band Operated Business | 38,000 | 40,000 | 50,000 | 50,000 | 50,000 |

| Total Revenue | 5,253,000 | 5,915,000 | 7,913,000 | 8,070,260 | 8,230,665 |

| Program Expenditures | |||||

| Economic Development | 78,000 | 90,000 | 105,000 | 105,000 | 105,000 |

| Social Development | 737,000 | 750,000 | 1,104,000 | 1,104,000 | 1,104,000 |

| Capital and Housing | 1,027,000 | 1,050,000 | 1,397,500 | 1,397,500 | 1,397,500 |

| Band Administration | 1,224,000 | 1,250,000 | 1,325,000 | 1,325,000 | 1,325,000 |

| Health | 550,000 | 650,000 | 770,000 | 770,000 | 770,000 |

| Education | 1,937,000 | 1,950,000 | 2,675,000 | 2,675,000 | 2,675,000 |

| Trust Funds | 0 | 0 | 0 | 0 | 0 |

| Other – Specify | 0 | 0 | 0 | 0 | 0 |

| Total Expenditures | 5,553,000 | 5,740,000 | 7,376,500 | 7,376,500 | 7,376,500 |

| Planned Surplus (deficit) | (300,000) | 175,000 | 536,500 | 693,760 | 854,165 |

| Use of Surplus | |||||

| Loan Repayments Account | -50,000 | -100,000 | -200,000 | -350,000 | |

| Accounts Payable Arrears | -50,000 | -130,000 | -100,000 | ||

| Deficit Reduction | -75,000 | -306,500 | -393,760 | -504,165 | |

| Surplus (Deficit) at Year End | -1,200,000 | -1,125,000 | -818,500 | -424,740 | 79,425 |

Annex C: MAP Form C: Capacity Development Plan – Completed Example

| Key Position |

Training/Staffing Activity |

Desired Outcome (in support of Objective per Form A) |

Training/Service Provider |

Responsible Person and Target Date |

Estimated Cost |

|---|---|---|---|---|---|

| Payroll Clerk |

Hire a qualified payroll clerk with experience |

Ensure payroll is paid on time with appropriate deductions to authorized employees only for actual hours worked. | Hire a Temp Advertise locally Target XXX community college Grads |

Band Manager & Finance Director

Immediate for Temp March 31, 2013 for staff |

$3500 per month |

| Personnel Director |

Labor Standards Act Employment contracts | Reduce/eliminate wrongful dismissal claims | Check Provincial Training Institute |

Personnel Manager. Complete by June 30, 2013 |

$1200 per month |

| Chief and Council |

Strategic Governance |

Ability to complete long- term community plan and 5 year business plan | AFOA | Office Manager Complete by Dec 31, 2013 |

$6000 per month |

Annex D: Checklist

All components of the MAP set have been effectively and comprehensively addressed as set out below.

- Recipient notified of requirement to develop and implement MAP due to funding agreement default or other cause.

- Any response to notice by the recipient has been considered.

- Annex A - Form A Action Plan has been completed in full.

- Annex B - Form B Financial Plan has been completed (if required).

- Annex C - Form C Capacity Development Plan has been completed (if required).

- Annex – Forms A, B & C represent a credible plan to address the defaults.

- The timelines proposed are reasonable and realistic and do not create undue risk or hardship for the service population.

- Use of proposed internal and external resources is appropriate and reasonable to execute the action plan.

- The recipient is informed, willing and able to execute the MAP.

- A reporting cycle has been established for the plan.

- An exit strategy has been developed for the plan.